View this page in: Portuguese| Spanish

The challenges of IFRS 17 in Latin America – Brazil and Peru in perspective

Authors: Gisele Sterzeck, PwC Brasil Partner and Sarah Arbieto, PwC Peru Senior manager.

The insurance market in Latin America

The new accounting standard IFRS 17 – Insurance Ccontracts has brought several challenges to insurance companies in its implementation. Still, it is an opportunity for these companies to rethink their processes from an operational and management point of view, considering that the generation of quality data to carry out the transition process is critical to have financial statements compliant with the new standard.

The insurance market in Latin America is diverse. While some countries have reasonable growth rates, others have a more stable or even stagnant performance. Of the total premiums paid in the Latin American market in 2019, approximately 54% came from non-life and 46% from life products1.

Another relevant feature of this market is that supervisory entities make their regulation with prudential policies somehow depart from what is required by international accounting standards in some cases.

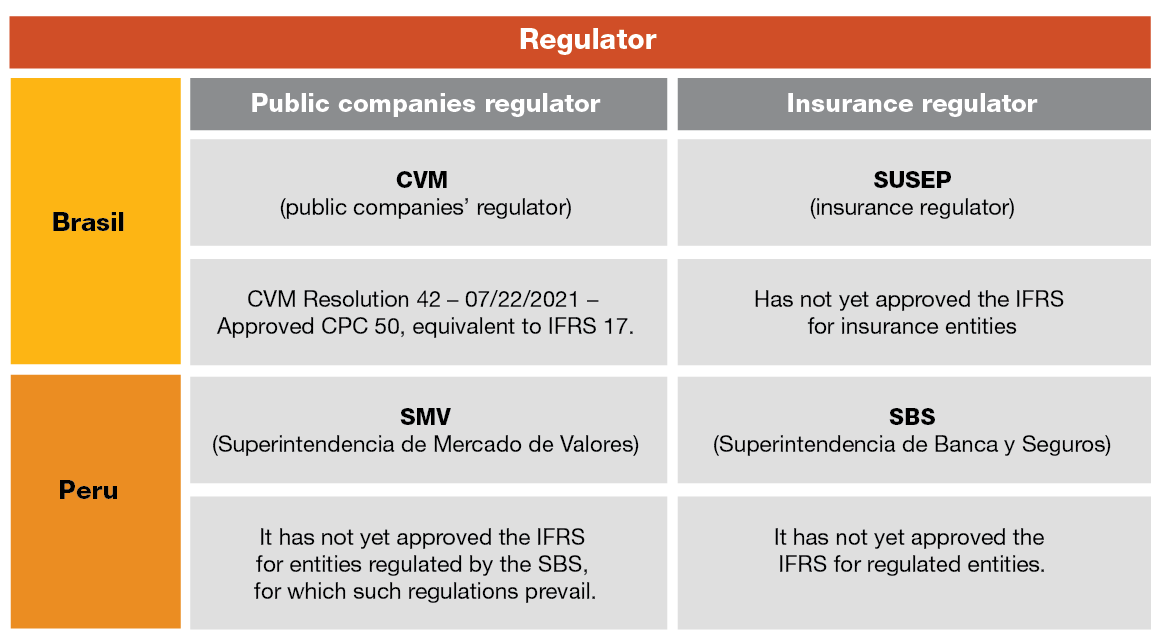

Local regulators need to approve international accounting standards before requiring them to be applied by regulated entities. Below is the current approval status in Brazil and Peru:

Subsidiaries of financial groups domiciled in the United States or Europe make up a large part of the insurance segment in Latin American countries. In some cases, these companies have recently started operating and are growing in an increasingly significant market in the region.

The challenges of IFRS 17

The implementation of the new accounting standard has several positive aspects, such as the improvement in the comparability of financial statements and the consistency with ccounting in other countries.

However, this process also creates some challenges for insurers. Below, we highlight some points that we have observed in Brazil and Peru regarding the implementation process:

In the case of small subsidiaries of foreign groups, requests to analyze the impacts of IFRS 17 arrived with some delay and with unclear guidelines.

Corporate guidelines will often have to be localized or adapted to the reality of each subsidiary and country, which creates an additional challenge for the group and the subsidiary.

Local teams also face challenges in training people dedicated to this type of project and often have to reconcile the project with accounting closing routines.

Expected and actual cash flows may differ in a separate, consolidated financial view, which may require independent calculations to be performed.

Some of the additional complexities related to transition methods, given that entities locally do not prepare separate financial statements following IFRS. They are often prepared in local GAAP.

How to address these issues?

The approaches to these issues are diverse and usually based on the work of external consultants or internal training and capacity building.

In the case of entities that are not part of foreign economic groups, the work of identifying gaps and seeking specialized support (consultants, auditors, etc.) may be more advanced, both regarding methodological definitions and the analysis of the feasibility of possible changes or system developments.

The experience of the consulting teams is also varied and responds to the needs of each country. In Peru, for example, the local regulator is interested in understanding the technical challenges involved in IFRS 17. However, as opposed to what happened in Chile, no initial impact assessment has been done or a regulatory requirement issued about the gap analysis.

In Brazil, the regulator also assesses the standard and has not requested any formal analysis or diagnosis for insurers. On the other hand, insurers that are considered public entities and subsidiaries of foreign companies are involved in more advanced implementation processes and discussions.

Implementing IFRS 17 can be very complex for insurers, bringing them both challenges and diverse opportunities to perform internal training or even hire consultants, who can present the different market insights on certain topics, must be well defined in the IFRS 17 project strategy. It will be essential for the success of the initiative.

1. The Latin American Insurance Market in 2019 – Fundación Mapfre.

Contatos